Traditional and Roth IRAs - Taking Retirement Into Your Own Hands

Traditional and ROTH IRAs

It is extremely important that we all take our retirement into our own hands. The concept of not preparing and relying on a government-sponsored retirement might not be the best plan. Financial woes combined with the fact that the U.S. population is continuing to age, means that there are fewer working-aged people remaining to contribute to our Social Security systems. On a positive note, strong retirement savings can not only help you, but it could potentially help your family and loved ones. With today’s retirement challenges, more people are using retirement vehicles as a healthy way to help family members. As advisors, we get great satisfaction helping parents and grandparents contribute to their loved ones lives by properly gifting funds to a retirement account (if the loved one has earned income and qualifies). Most financial professionals can agree that consistently funding your retirement plans is a healthy activity. Funding retirement accounts at younger ages can increase your chances of a better funded and more comfortable financial situation at your retirement.

You can contribute to your 2020 IRAs, but thanks to the CARES Act, you can still make 2019 IRA contributions until July 15, 2020. In 2019 and 2020, the limit for contributing to an IRA is $6,000. Now is also a good time to consider making your 2020 retirement contributions.

For complete rules on IRA’s (including who qualifies), please visit www.irs.gov Publication 590a or consult with a qualified professional. Here is some timely information that may be helpful. To discuss your overall retirement strategy please call us and schedule an appointment.

Traditional IRAs

A traditional IRA (Individual Retirement Account) is a way in which individuals can save for retirement and receive tax advantages. Traditional IRAs come in two varieties: deductible and nondeductible. The contributions you make to a traditional IRA may be fully or partially deductible, depending on your circumstances (i.e. taxpayer's income, tax-filing status and other factors) and generally, amounts in your traditional IRA (including earnings and gains) are not taxed until they are distributed.

A clear advantage of traditional IRA accounts is that you can benefit from deferring taxes on all dividends, interest and capital gains earned inside the IRA account and they can potentially compound each year without being reduced by taxes. This may allow an IRA to have faster growth potential than a taxable account.

Roth IRA

A Roth IRA is an IRA that is subject to many of the same rules that apply to a traditional IRA with some major exceptions. Unlike traditional IRAs which for some taxpayers can be tax deducted, you cannot deduct contributions to a Roth IRA. Some Roth IRA advantages include:

- If you satisfy the requirements, qualified distributions are tax-free.

- You can leave funds in your Roth IRA for your entire lifetime.

- Beneficiaries inherit your Roth IRAs tax-free, if account requirements have been satisfied.

Many investors know and understand that the largest benefit of the Roth IRA is its tax-free withdrawal of contributions, interest and earnings in retirement, but Roth IRAs can also help you leave a legacy to your heirs with proper estate planning.

Are you interested in funding an IRA for you or a family member? If so, please call us and we would be happy to assist you.

Spousal IRA

If your spouse doesn't work, they can still have a spousal traditional or Roth IRA. This allows non-wage-earning spouses to contribute to their own traditional or Roth IRA, provided the other spouse is working and the couple files a joint federal income tax return. If the working spouse is covered by a retirement plan at work, deductibility of contributions to a spousal traditional IRA would be phased out at higher incomes. Eligible married spouses can each contribute up to the contribution limit each year to their respective IRAs (spousal IRAs are also eligible for a $1,000 catch-up contribution for those 50 and older). To discuss spousal IRA strategies, call us.

Custodial Roth IRA

Starting retirement savings early can allow you the potential advantage of growing money in a tax efficient account over a long period of time. Many children work before they reach age 18. The income they earn makes them eligible to contribute to a Roth IRA, which can be an extremely smart move for teenagers. This can also provide an excellent opportunity for you to teach or reinforce with your children the importance of saving money.

Some of the rules regarding custodial Roth IRAs are:

- To be eligible to open a custodial Roth IRA, the child must meet all the same requirements as an adult. The minor must have earned income and contributions are limited to the lesser of total earned income for the year and the current maximum set by law, which for 2019 and 2020 is $6,000.

- Adjusted gross income for the child must be below the thresholds above which Roth IRAs aren't allowed.

- Even though the custodian is the legal owner of the account, the Roth IRA must be managed for the benefit of the minor child.

- As the custodian, you make the decisions on investment choices—as well as decisions on if, why, and when the money might be withdrawn—until your child reaches “adulthood,” defined by age (usually between 18 and 21, depending on your state of residence). Once they reach that age, the account will then need to be re-registered in their name and it becomes an ordinary Roth IRA.

If you're the parent of a child who has earned income, a Custodial IRA can be a great way to teach the value of saving and investing. Besides getting a head start on saving, your child may be able to use the funds for college expenses—or even to buy a first home.

There are several ways to fund a Custodial Roth. For example, you can potentially use your annual ability to gift to children or grandchildren to make this happen. If your child or grandchild is earning money, call us to discuss options for setting up a Custodial Roth.

"Back-door" Roth IRA

The traditional contribution ("front door") for Roth IRAs is currently not available for higher income earners. Married couples earning $206,000 or more and singles earning $139,000 or more in 2020 are still fully excluded from contributing directly to Roth IRAs.

In 2010, Congress changed the rules and since then anyone can convert a traditional IRA to a Roth IRA. However, higher income earners are still ineligible to contribute to a Roth IRA. A Backdoor Roth IRA is a strategy for some higher income earners to participate in Roth IRAs. It is a way for higher income earners to put money into a traditional IRA and then roll that into a Roth IRA, getting all the benefits. While this strategy sounds simple, there are several rules that you must know and follow to make sure you do not incur unintended tax consequences. This is where working with a knowledgeable financial or tax professional can provide guidance and value.

Custodial Roth IRA

The Backdoor Roth conversion can consist of two simple steps:

- You make a nondeductible contribution to your traditional IRA.

- Then, after consulting with your financial advisor or tax professional, you convert this IRA into a Roth IRA.

There's one big caveat: This strategy may work best tax-wise for people who don't already have money in traditional IRAs. That's because in conversions, earnings and previously untaxed contributions in traditional IRAs are taxed—and that tax is figured based on all your traditional IRAs, even ones you aren't converting. (Please read the section on the Pro Rata Rule.)

For an investor who doesn't already hold any traditional IRAs, creating one and then quickly converting it into a Roth IRA may incur little or no tax, because after a short holding period there's likely to be little or no appreciation or interest earned in the account. However, if you already have money in traditional deductible IRAs, you could face a far higher tax bill on the conversion (again, this is covered later in the section on the Pro Rata Rule).

If you choose to attempt a backdoor Roth IRA conversion, please consult a knowledgeable tax planner prior to doing so because the rules for Roth conversions can be complicated.

The SECURE ACT and the 10-year Rule

If you have saved a lot for retirement, or your parents have, you could be affected by recent changes in the rules about retirement distributions.

The Secure Act passed on December 20, 2019 eliminated the “stretch IRA,” a strategy used by retirement account owners to pass tax-advantaged money to their heirs. The “stretch IRA” allowed non-spouse beneficiaries like children and grandchildren to take money out of an inherited IRA gradually over their lifetimes. This new law (SECURE Act) requires most IRAs inherited by people other than spouses to be depleted within 10 years, which can sometimes lead to much higher tax bills for heirs. (Spouses still have the option of treating an inherited IRA as their own and taking money out over their lifetimes.)

For some IRA owners it might make sense to do a partial or even complete conversion to a ROTH IRA before leaving this asset to an heir. This decision can be a complicated one and we suggest talking with your financial professional and tax preparer about your situation. To discuss your situation, please give us a call.

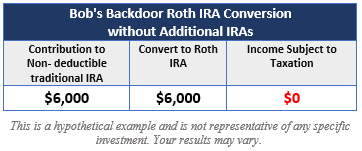

Example of a Backdoor Roth IRA

Bob, a high-income earner, decides on January 2nd to put $6,000 into a traditional IRA. Bob's income is too high to be able to deduct these contributions from his taxes. After consulting with his financial advisor or tax advisor, he then converts the traditional IRAs to Roth IRAs completely tax-free. His income is too high for him to make a direct contribution into a Roth IRA, but there’s no income limit on conversions. Since Bob couldn’t deduct the contribution anyway, he might as well get the advantage of never paying taxes on that money again available through the Roth IRA.

Beware of the Pro Rata Rule for Roth Conversions

The Pro Rata rule for Roth conversions states that if you have any other deductible IRAs (i.e. a previous 401k that you’ve rolled over), the conversion of any contributions becomes a taxable event that you’ll need to pay taxes on upfront.

The Pro Rata rule for Roth conversions determines whether your conversion will be taxable. For taxation purposes, the IRS will look at your entire IRA holdings (even if they are in different accounts), not just the traditional IRA you are converting to a Roth IRA and will determine what your tax bill will be based upon a ratio of IRA assets that have already been taxed to those IRA assets in total.

The IRS determines the tax on this conversion based on the value of all your IRA assets. For example, Peggy, a high-income earner, already has $94,000 in an IRA account, all of which has never been taxed. She decides on January 2nd to put $6,000 into a new traditional IRA. The next day she converts the new traditional non-deductible IRA to a Roth IRA. Peggy’s income is too high for her to make a direct contribution into a Roth IRA, but there’s no income limit on conversions. She has $94,000 in other IRAs (previously non-taxed), so her total IRA assets are now $100,000. When she converts $6,000 to a Roth IRA, the IRS pro-rates her tax basis on the previous taxation of her total IRA assets, therefore making this conversion 94% taxable ($94,000/100,000 = 94%).

If you plan on using this backdoor IRA strategy, you want to be clear as to whether or not you have any other IRAs. As you can see, this can be a confusing area, and this is where we can help. If you are a high-income-earner we would be happy to review your situation to determine if this strategy is in your best interest.

Also, please remember that your spouse’s IRA is separate from yours.

Am I a Candidate for a Backdoor Roth IRA?

Backdoor Roth IRAs can be appropriate for investors who:

- Only have retirement accounts through their jobs (i.e. 401k's) and want to increase their retirement savings in tax-advantaged accounts, but whose income is too high to qualify for standard Roth IRA contributions; and

- Have the time and ability to wait for five years or until they are 59 ½, whichever is later, to avoid the 10% penalty on early withdrawals.

A Backdoor Roth IRA is probably not recommended if you:

- Don’t want to contribute more than the maximum retirement limit through your workplace retirement account.

- Already have money in a traditional IRA and because of the Pro Rata rule may end up in a non-tax advantageous position when converting to a Backdoor Roth IRA.

- Plan or expect to withdraw the funds in the Roth IRA within the first five years of opening it. A Backdoor Roth is considered a conversion and not a contribution. Therefore, the funds may incur a 10% penalty if withdrawn within five years no matter your age.

- Are in a high tax bracket now and expect to be in a lower tax bracket in the future.

- Plan to relocate to a lower or no income tax state.

Note: While Backdoor Roth IRAs can be beneficial to many investors, they aren’t for everyone. They come with their limitations and complications. There are precautions that need to be taken to reap the full benefits of any financial decision. Please consult and review your situation with a qualified professional prior to choosing to use this strategy.

We are here to help.

If you have an interest in further discussing funding your retirement plans, please call us. This is an area where a highly informed financial advisor can help you make an educated and calculated decision. As with all tax sensitive decisions, you should always consult with a wealth advisor and tax professional to help avoid tax ramifications. At Prestige, we have both of these professionals all under one roof to help you with your specific financial situation.

We enjoy the opportunity to assist clients in addressing all financial matters. You can conveniently schedule a complimentary consultation with us by clicking below.

This article is for informational purposes only. This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice as individual situations will vary. For specific advice about your situation, please consult with a lawyer, tax or financial professional. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation.

Contributions to a traditional IRA may be tax deductible in the contribution year, with current income tax due at withdrawal. Withdrawals prior to age 59 ½ may result in a 10% IRS penalty tax in addition to current income tax. Traditional IRA account owners should consider the tax ramifications, age and income restrictions in regards to executing a conversion from a Traditional IRA to a Roth IRA. The converted amount is generally subject to income taxation. The Roth IRA offers tax deferral on any earnings in the account. Withdrawals from the account may be tax free, as long as they are considered qualified. Limitations and restrictions may apply. Withdrawals prior to age 59 ½ or prior to the account being opened for 5 years, whichever is later, may result in a 10% IRS penalty tax. Future tax laws can change at any time and may impact the benefits of Roth IRAs. Their tax treatment may change. IRA’s and ROTH conversions require understanding of specific rules, for complete rules on IRA’s (including who qualifies), please visit www.IRS.GOV Publication 590a or consult with a qualified professional. Source: www.irs.gov. Contents Provided by The Academy of Preferred Financial Advisors, Inc.; Reviewed by Keebler & Associates, Inc.