Newsletter - 3rd Quarter 2020

RECAP

Broad equity markets trended higher for the third quarter. Equities continued to improve during the months of July and August as the U.S. economic data showed improvement as a result of the Fed’s monetary policy and the government’s fiscal stimulus that were provided at the height of the COVID pandemic. However, a modest pullback ensued in September as market participants became concerned that an agreement for a second stimulus bill would not be reached. The upcoming U.S. presidential and senate elections also contributed to investor anxieties about the uncertainty surrounding future regulatory and tax policies and the impact that they could have on capital markets.

FEDERAL RESERVE POLICY CHANGES

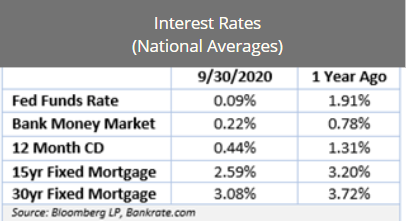

During the quarter, the U.S. Federal reserve pledged to keep interest rates low until at least 2023. Fed Chair Powell announced that the Fed will change its approach to targeting inflation from a direct 2% level to an average inflation targeting of 2% which would effectively allow inflation to run within a range of 1% to 3%. This is a stark change from its previous policy which triggered rate hikes when inflation started to run above the 2% level. Many economists believe that this added flexibility will help create a more sustainable recovery but could also contribute to higher inflation in the short run. Additionally, the Fed shifted its approach to employment that will now focus on the lower end of the income spectrum as opposed to the overall level of employment. A move that many believe should aid in the income equality that had been created by some of its prior policies during the last recession.

The Fed reduced some of its bond purchasing for the quarter but still maintained the same $7 trillion balance sheet with which it started in July. Although many of the Fed members hinted at additional monetary stimulus, they are adamantly awaiting Congress’s fiscal stimulus before acting.

US AND GLOBAL ECONOMY

The U.S employment picture remarkably improved for the quarter with the September’s rate of unemployment registering at 7.9%. This is a substantial drop from the 14.7% level that was reached back in April and below the 10% peak of the Financial Crisis that was reached in October of 2009. Although all of the employment sectors have experienced declines in their levels of employment since February, the two sectors that have been most affected by the aftermath of the pandemic are mining & lodging and leisure & hospitality which still have unemployment levels at 14.2% and 22.8% respectively. These sectors together have contributed to over 30% of the current unemployment rate.

Low mortgage rates fueled housing demand for the quarter with August posting record contract signings according to the National Association of Realtors. Home prices across all four U.S. regions increased by almost 11% on average from a year ago as unsold inventories shrunk to just a 3-month supply. Of course, inventories have been impacted mostly by the 30% decline in new listings. Sales were up 10.5% from a year ago which is a strong sign that consumer confidence is starting to return.

U.S. GDP is expected to increase by over 35% for the quarter according to Atlanta Fed estimates. This rebound is also being confirmed by the recovery of both global manufacturing- and service-based purchasing manager indexes (PMIs). As of August, these indexes registered 51.8 and 51.9 respectively where readings above 50 indicate an expansion.

US EQUITY MARKETS

Equity markets continued to remain expensive on a historical basis. Especially when evaluating prices in context to the current year’s earnings. Many equity analysts have given earnings for this year a pass and are now looking out to 2021 and 2022 earnings as anchors to current valuations. According to economist, Dr. Edward Yardeni, earnings for the S&P 500 are expected to increase by 24% next year. This will still put the earnings total close to 2019’s tally, which may still not seem to justify current prices from a traditional standpoint. However, with extremely low interest rates, international market concerns and ample liquidity, investors continue to remain supportive of U.S. stocks.

U.S. stocks continued their trend of outperforming international stocks on both a quarterly and annual basis. U.S. small-cap stocks reversed their prior quarter trend and underperformed large-cap stocks for the quarter. Growth stocks also continued to dominate value stocks across all market capitalization sizes. The concerns regarding additional fiscal stimulus and confirmation of a sustained recovery contributed to these performance differences in the more economically sensitive segments of the equity market. For international markets, the emerging market segment outpaced their developed market peers for the quarter once again. China was again the largest contributor to emerging market returns despite increased tensions with the U.S. The U.S. Commerce Department placed restrictions on Huawei governing their use of semiconductor technology and the Trump Administration forced ByteDance to divest its TikTok U.S. operations over security concerns.

FIXED INCOME MARKETS

U.S. aggregate bond yields were little changed from the prior quarter ending September at just 1.18%. Some of the risker areas of the bond market continue to offer much higher yields than the broad bond market and we have been prudently repositioning some of the portfolio to these segments. However, the historically low yielding environment has called to question the relevance of fixed income within a portfolio as of late. Our response to this inquiry comes with two points: First, U.S. diversified bond yields continue to offer the most attractive yields globally when compared to other developed market yields. Especially when considering credit and currency risk. Second and most importantly, bonds still offer investors a key diversification benefit by helping to reduce volatility when stock prices fluctuate.

MARKET OUTLOOK

Several risks still loom for U.S. markets as we finish the year. The Fall and Winter months could foster targeted shutdowns should COVID cases spike. Although we believe that the extent of potential shutdowns would be less restrictive than the measures imposed at the start of the pandemic. Congress’s delay in passing its stimulus bill could also stymie the recovery that has persisted for the last two quarters. And finally, the upcoming presidential election may contribute to equity market volatility. Especially if the election results were to become contested.

Although the outcome of the election could impact market returns in the short term, we want to caution investors against basing their investment decisions exclusively on the results. Regardless of one’s political affiliation, it is important to recognize that even though market returns may vary in the short run depending on a party retaining or coming to power, the returns over the long-term have been consistent across all scenarios. The adjacent chart highlights this best. In the subsequent two years of a presidential election, market returns did vary significantly. However, the proceeding four-year period shows total returns that are fairly close. Also, markets never operate in a vacuum. The influence of the Federal reserve, current regulatory environment and industry specific trends will always be competing forces of politics.

Despite these near-term risk factors, it is always important to remember that markets are not driven exclusively by one event or force. Jeremy Siegel, the Wharton professor, who is credited for predicting that the DOW would cross 20,000 in 2015, explained to CNBC in an interview on September 28th why he believes that the stock market, “is looking forward to a really good run next year,” regardless of who takes the White House. Dr. Siegel explained that the “tremendous burst of liquidity” from the Fed and Congress will continue to provide a tailwind for stocks. He also added that uncertainty will continue to weigh on markets.

DISCUSS YOUR CONCERNS WITH US

Equity investors need to have realistic time horizons and return expectations. Predicting short-term changes in the markets is near impossible. Therefore, creating an investment plan that identifies your goals and time frame are important. We always like to say that panic is not a plan. If you have carefully created a strategy with realistic goals, then try not to allow the media’s influence or your emotions change your approach.

Our advice is not one-size-fits-all. We will always consider your feelings about risk and the markets and review your unique financial situation when making any recommendations.

At Prestige, we design custom portfolios with the goal to both protect and grow your wealth. Our wealth advisors are ready to help you with an obligation free complimentary review of your portfolio. If it's good, we'll tell you. If it's not, we'll provide feedback on things that can help. Click below to schedule your complimentary review today.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Prestige Wealth Management Group, LLC), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Prestige Wealth Management Group, LLC. Please remember to contact Prestige Wealth Management Group, LLC, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services. Prestige Wealth Management Group, LLC is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of the Prestige Wealth Management Group, LLC’s current written disclosure statement discussing our advisory services and fees continues to remain available upon request.